July 11, 2017

D Ward Insurance

Home Service Line Coverage – Protect Your Pipes!

D. Ward Insurance is proud to announce that Auto-Owners, one of its insurance carriers, now offers Service Line Coverage. Service Line Coverage provides protection against a leak, break, tear, rupture, collapse or arcing of a covered service line caused by the following perils:

· Wear and tear

· Marring

· Deterioration

· Hidden decay rust or other corrosion

· Mechanical breakdown (latent defect or inherent vice)

· Weight of equipment or animals or people

· Artificially generated electrical current

· Freezing or root invasion

What are some examples of covered property?

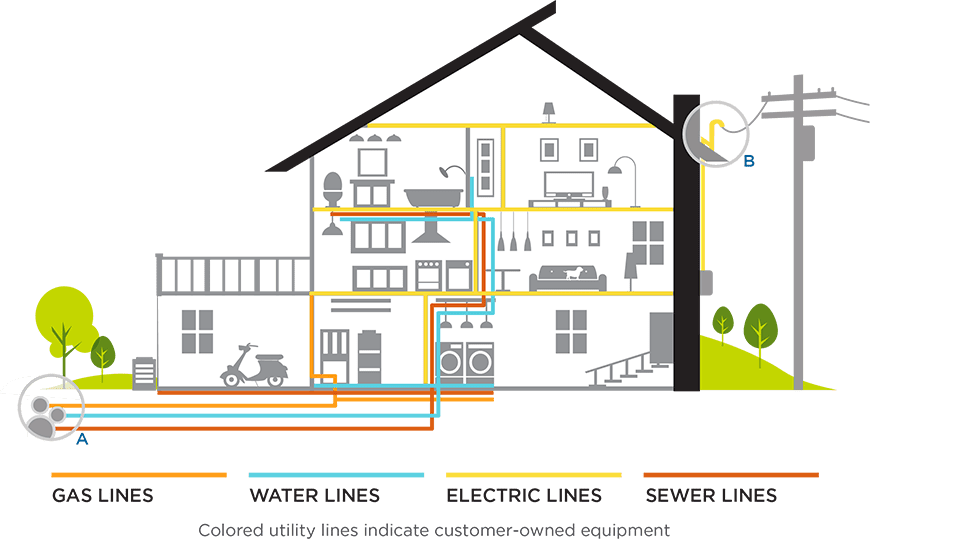

Service Line Coverage applies to the following underground properties:

· Water piping that connects from the residence to a public water supply system or private well system

· Loop piping that connects to a heat pump

· Sewer piping that connects from the residence to a public sewer system or private septic system

· Power line that provides electrical service to the residence premise

Does my line qualify for Service Line coverage?

In order to qualify for Service Line coverage, the line in question must be located on the residence premise, must provide a service to the residence as defined in the endorsement, and must be owned by the insured or the insured must legally be liable for repair or replacement.

How much coverage can I expect from Service Line coverage?

If the line or lines qualify, the deductible is $500 per occurrence with a $10,000 limit per occurrence. Excavation costs are covered up to the $10,000 per occurrence limit. However, blockage or low pressure of a service line is not covered as there is no direct damage to the line.

I was digging on my property and damaged my service line. Am I covered?

Impact from digging is not a named peril. However, this endorsement extends coverage for collapse as a result of the weight of equipment that could be used in the course of digging.

What underground piping does Service Line coverage exclude?

Service Line coverage does not cover every underground pipe and wire. Exceptions to coverage include underground piping to outdoor property, including but not limited to: sprinklers, irrigation systems, swimming pools, hot tubs and decorative ponds.

Service Line coverage does not extend to wiring that provides electricity to outdoor property such as light fixtures and electric fencing, or piping or wiring that is not connected and ready for use. Other examples of non-included items are storm water drain piping, water wells, including well pumps or motors, and heating and cooling equipment like heat pumps. Underground piping to the residence including Geothermal piping would be considered covered property, however.

Tree roots damaged my sewer line, and now I have to remove the tree. Does Service Line coverage apply here?

Outdoor property, such as trees, shrubs, plants, lawns, walkways, and driveways, that is damaged as a result of a service line occurrence or damaged during the excavation of the service line would be covered within the $10,000 per occurrence limit.

Something off my property blew up and damaged my service line. Am I covered in this instance?

Coverage would not apply in the case of off-premise explosions, as it would not meet the criteria for named perils listed in the endorsement.

I have a natural gas line providing service to my home. Is it included in Service Line coverage?

Coverage would be provided as long as the natural gas line is underground, is on your premise, provides a service to your premise, and experiences an occurrence.

D. Ward Insurance would be happy to answer any questions you may have about Service Line coverage or to begin the process of getting a Service Line endorsement. Call us today at 770-974-0670 or visit dwardinsurance.com to request a quote. We look forward to doing business with you!

Disclaimer: This report is for information purposes only and is not to be construed as definitions of policy coverages or limits. This report does not alter, amend, or change the policy wording and the intent of this report is to bring attention & to have a conversation with D. Ward about your insurance needs.

Categories: Blog